In 2025, the NEV market is exhibiting a relatively complex development trend, with its inventory situation reflecting various market characteristics.

As of the end of May 2025, the total inventory of the national passenger vehicle industry reached 3.45 million units, a decrease of 50,000 units MoM, but an increase of 160,000 units compared to the same period in 2024. According to the CPCA, the inventory of passenger vehicles from NEV manufacturers rose from 660,000 units in December 2024 to 880,000 units in May 2025. However, in terms of the inventory coefficient, the comprehensive inventory coefficient of auto dealers in May 2025 was 1.38, down 2.1% MoM and 4.2% YoY.

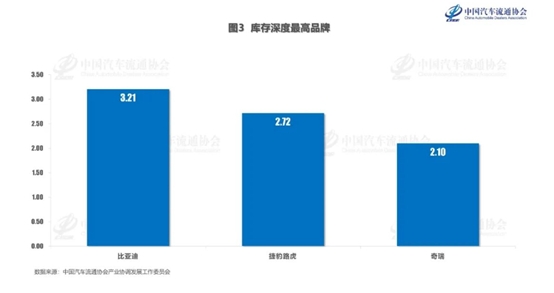

Meanwhile, some brands have higher inventory coefficients. The three brands with the deepest inventory in May 2025 were BYD, Jaguar Land Rover, and Chery. Among them, BYD, as a representative brand in the NEV sector, has a relatively high inventory coefficient. According to data from the China Automobile Dealers Association, BYD's inventory is equivalent to 3.21 months of sales, reflecting high market attention for its products but also indicating certain inventory pressure.

The risks posed by high inventory cannot be underestimated. The inventory scale of 3.45 million units has reached a new high in nearly two years, with the increase in inventory from NEV manufacturers directly translating into financial pressure and operational risks for dealers. The depreciation of inventory vehicles, rising capital occupation costs, and potential risks of slow sales are all testing the resilience of dealers. For NEV enterprises, it is crucial to reasonably control inventory. On the one hand, they should flexibly adjust production plans based on market demand to avoid inventory backlogs; on the other hand, they should accelerate inventory turnover and reduce operational risks by optimizing sales channels and enhancing product competitiveness.

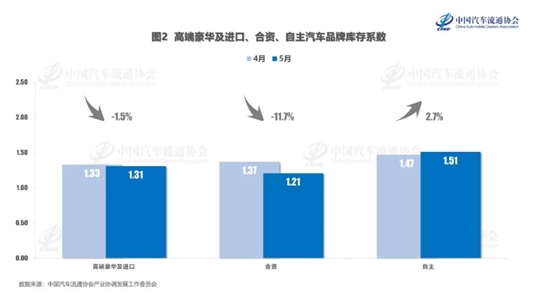

In May 2025, the inventory coefficient of high-end luxury and imported brands was 1.31, down 1.5% MoM; the inventory coefficient of joint-venture brands was 1.21, down 11.7% MoM; and the inventory coefficient of domestic brands was 1.51, up 2.7% MoM. Some NEV brands, such as BYD, have higher inventory coefficients, while some traditional luxury brands, like Jaguar Land Rover, have not effectively improved their overall inventory situation with the market performance of their NEV car models, reflecting the fierce competition in the NEV market and the development disparities among brands. Based on the current wholesale sales data from May to June, the market exhibits distinct structural characteristics and complex trends. The inventory of mainstream independent automakers has risen significantly compared to the end of last year, reflecting automakers' positive expectations for market growth in 2025 and a relaxation of inventory safety measures. Meanwhile, the inventory of luxury cars has also increased, while the inventory of foreign brands remains relatively stable.

Despite the current strong growth momentum in the automotive market, the arrival of the traditional off-season from June to August will have a certain inhibitory effect on market sales. From the inventory perspective, a higher inventory cycle implies that the industry needs to reasonably control the pace of production and sales. In the future, with the further development and intensified competition in the NEV market, various brands will need to pay more attention to inventory management to achieve sustainable development.

SMM New Energy Industry Research Department

Cong Wang 021-51666838

Xiaodan Yu 021-20707870

Rui Ma 021-51595780

Disheng Feng 021-51666714

Yujun Liu 021-20707895

Yanlin Lü 021-20707875

Zhicheng Zhou 021-51666711

Haohan Zhang 021-51666752

Zihan Wang 021-51666914

Xiaoxuan Ren 021-20707866

Jie Wang 021-51595902

Yang Xu 021-51666760

Boling Chen 021-51666836